How Blockchain Works: A Complete Guide

17 March 2026 • 23 Min ReadYou’re not the only one who has ever wondered how blockchain works. People use the word all the time—in the news, in crypto conversations, and even in boardrooms. strategy meetings—but most explanations are full of jargon before you can even get your bearings. Let’s improve that.

The most basic definition of blockchain is a way to keep records that no one can change secretly. Imagine a notebook that thousands of people are copying at the same time. Each new entry has to be approved by the group before it is written down. No one is in charge, there is no eraser, and no edits are made in the back room. That’s the main point.

This guide covers blockchain technology, transaction verification, and real-world business use. You can get clear, no-nonsense answers here, whether you’re new to crypto or just want to learn more.

What is the technology behind blockchain?

Blockchain technology is a digital record book that is stored on thousands of computers at once. Every person on the network has a copy of the master copy, not just one company or government. Every copy updates automatically and almost instantly when new information is added.

Each piece of information is called a “block.” Each block has a time stamp, a batch of confirmed transactions, and a unique code that links it to the block before it. When you put them all together, you get a chain of blocks, which is where the name comes from.

There are three things that make the whole thing work. First, distribution: the data is spread across many machines rather than being stored in a single location that could be compromised. Second, cryptography: complicated math scrambles and protects data so that only people who have permission can read or sign it. Third, consensus: the network uses a set of rules that everyone agrees on to figure out which transactions are real and which ones aren’t. The system takes care of that part, so you don’t have to trust strangers.

This mix makes a record-keeping system that is open, safe, and can police itself. This is why blockchain technology has spread far beyond cryptocurrency to include things like tracking supply chains, keeping medical records, and creating digital identities. It is also the backbone of platforms like InstaXchange, which let you buy and sell crypto quickly and safely.

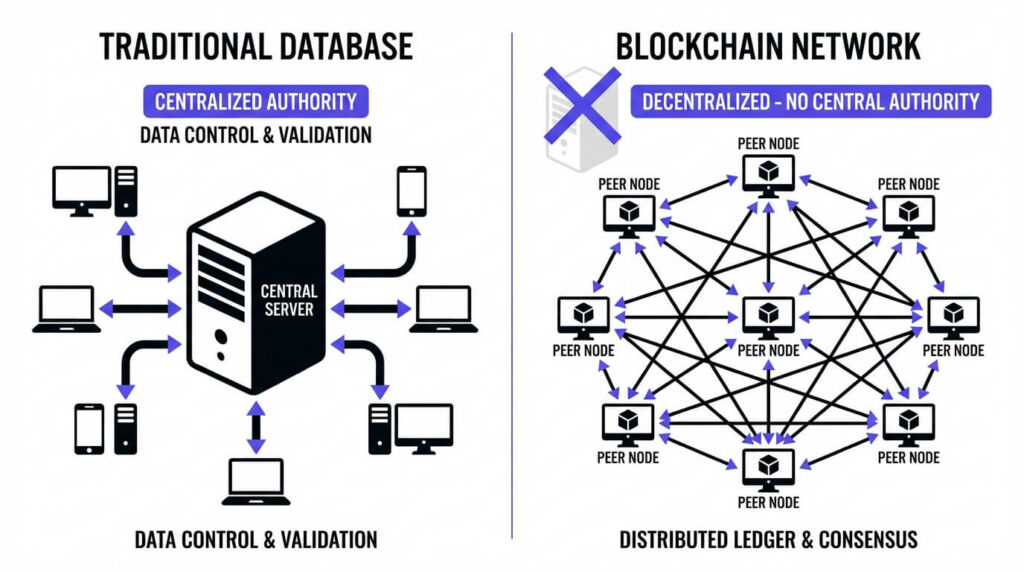

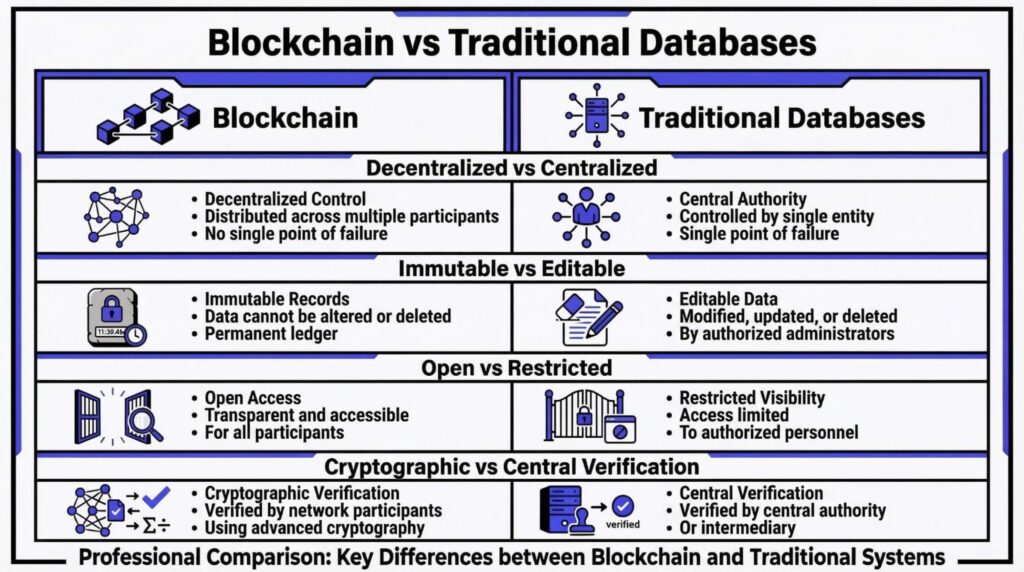

What makes blockchain different from regular databases

A normal database is like a spreadsheet that is stored on a company’s private server. One administrator, or a small group of them, decides who can access the records, what changes can be made, and when records can be deleted. If that administrator makes a mistake, gets hacked, or does something dishonest, all of the records in the system are in danger.

Blockchain turns that arrangement on its head. No one owns the ledger completely. Instead, everyone on the network checks changes together. Once a transaction is confirmed and added to a block, it stays there forever. There is no edit button, delete key, or way to change things behind the scenes. One of the main reasons people trust blockchain for big transactions is that it is permanent.

Another big difference is how visible they are. Most traditional databases don’t let you see how they work on the inside; you have to trust the operator that the data is correct. Anyone who is allowed to see the full history of transactions on a blockchain can do so. This creates a built-in audit trail that holds everyone accountable.

In short, blockchain replaces one person’s control with group agreement. You don’t trust an institution to be fair; you trust the math and the rules that are built into the network itself.

How Does Blockchain Work? (Step-by-Step Process)

It is much easier to understand how blockchain works when you divide the process into four clear steps. Each step builds on the one before it, making it possible for information to go from request to permanent record in a matter of minutes (and sometimes seconds).

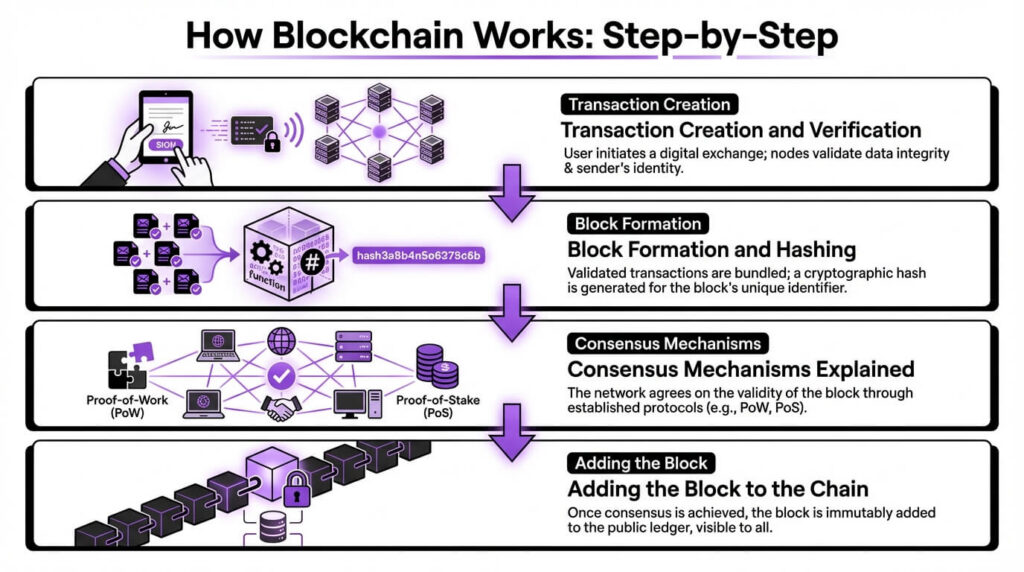

Step 1. Transaction Creation and Verification

When someone sends cryptocurrency, transfers ownership of a digital asset, or starts a smart contract, everything begins. That action makes a transaction that has all the important information, like who is sending, who is receiving, and how much is involved.

The sender’s private key makes a digital signature before the transaction can move forward. This signature is like a wax seal on an old letter. It shows that the message really came from you and that no one else can copy it.

The network then gets the signed transaction. Nodes, which are computers on the blockchain, pick it up and do a quick check to make sure everything is okay. Does the person sending the money really have enough? Is the signature real? Has this exact transaction already been sent in? If something doesn’t make sense, the transaction is immediately turned down. Only transactions that are clean and valid can go through.

This step of verification is one reason why your crypto purchases go through so quickly on InstaXchange. The blockchain handles authentication in real time, so you don’t have to wait for a bank or a middleman to sign off.

Step 2. Block Formation and Hashing

After a group of transactions have been checked, they are put together into a new block. Each block has three pieces of information: the list of valid transactions, a timestamp showing when the block was put together, and a cryptographic hash of the block before it.

A hash is like a digital fingerprint. You can put any piece of data into a hash function and get a string of characters that is always the same length and is different for each input. If you change even one letter in the original data, the hash changes completely. This means that anyone who looks at the numbers will see that something has been changed.

Here’s the smart part: each block has the hash of the block before it, so all the blocks are linked in order. If you change one old block, the fingerprint reference in every block that comes after it would break, like pulling a card out of a house of cards. This chaining is what makes it so hard to change the ledger.

The genesis block is the first block in a blockchain. Every other block in the chain comes from it.

Step 3. Consensus Mechanisms Explained

So, who decides if a new block is real? That’s when consensus mechanisms come into play. The whole network uses them to agree on what’s true and what’s not, and no one has to call or send an email to do so.

Proof of Work (PoW) and Proof of Stake (PoS) are the two most common methods.

In Proof of Work, people called miners compete to solve a very hard math problem. The first miner to solve it gets to add the next block to the chain and gets paid for their work. This is how Bitcoin works. It’s very safe, but it uses a lot of computing power and electricity.

Proof of Stake looks at things in a different way. Validators don’t solve puzzles; instead, they put up a piece of their own cryptocurrency as collateral (a “stake”). The network chooses validators to confirm new blocks in part based on how big their stake is. If a validator tries to cheat, they lose the money they put up as collateral. This is how Ethereum works now, and it uses a lot less energy than Proof of Work.

No matter what kind of mechanism a blockchain uses, the goal is the same: make sure everyone is honest and stop anyone from spending the same digital coin twice. The consensus layer is what makes the blockchain safe to use, even if the people using it don’t know or trust each other.

Step 4. Adding the Block to the Chain

When everyone on the network agrees, the new block is added to the end of the chain. Every node on the network updates its own copy of the ledger at the same time. This way, everyone is always looking at the same version of the truth. No records that don’t match up, no lag between offices, and no spreadsheets for reconciling.

From now on, the transactions in that block are set in stone. The blockchain grows one block at a time, and each new block makes everything that came before it safer.

Why Blockchain Data Is Immutable

People in the crypto world use the word “immutability” a lot, but the idea is simple: once data is written to the blockchain, it can’t be changed.

It all goes back to those cryptographic hashes. It would be necessary to recalculate the hash of that block and every block after it if you changed any one record. This is because the fingerprint of each block depends on the content of the block before it. Also, the attacker would have to take control of most of the nodes on the network to get those fake changes to go through consensus. It’s not just hard to do on a big public blockchain with thousands of nodes all over the world; it’s almost impossible.

This built-in resistance to tampering is exactly why financial platforms, governments, and healthcare systems are using blockchain for records that can’t be changed in any way.

Technical Aspects of Blockchain’s Core Features

Peer-to-Peer Networks and Decentralization

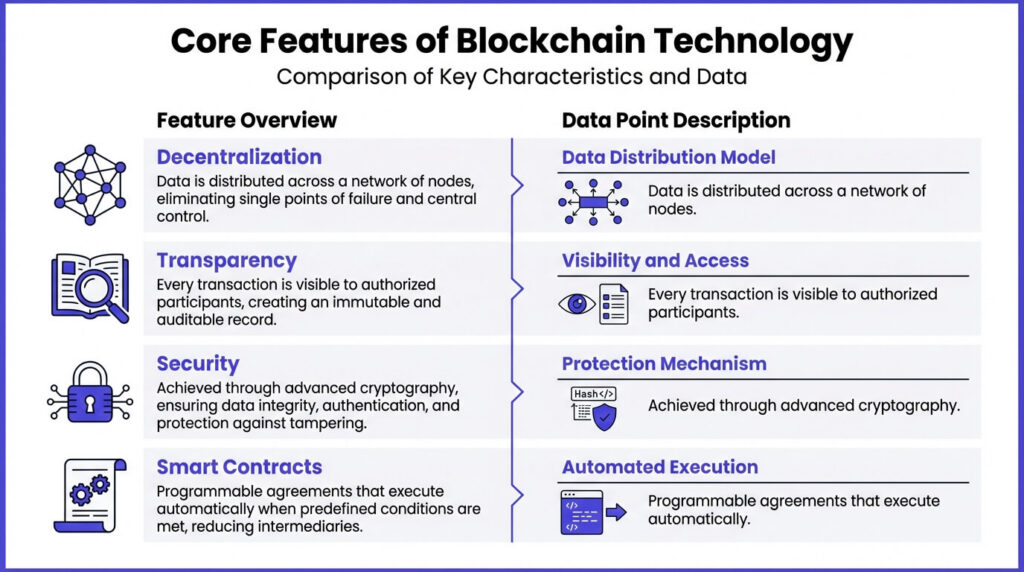

The philosophical core of blockchain technology is decentralization. Blockchain doesn’t send all of its data through a central server, which can go down or be hacked and take everything down. Instead, it sends data through a peer-to-peer network of independent nodes. There is no one node that has more power than the others, and each node has a full copy of the ledger.

This design makes the system very strong. The rest of the network keeps going even if a few nodes go down, whether it’s because of a power outage, a cyberattack, or routine maintenance. It’s like a group of birds that keeps flying even when some of them leave. The group changes shape and moves on.

Transparency and Distributed Ledgers

Anyone who has permission to see the blockchain network can see every transaction that has ever been recorded on it. That openness does something very powerful: it changes “trust me” to “check for yourself.”

When a new block is added, everyone’s copy of the ledger updates at the same time. Everyone sees the same things, the same timestamps, and the same order of events. This makes it easy to settle disagreements and audit because the proof is available for everyone to see.

That openness is important for a crypto exchange like InstaXchange. It means that every trade and transfer is recorded on the blockchain in a way that can be checked, which gives users peace of mind that their transactions are real and can be tracked.

Security Through Cryptography

Cryptography is the system of locks and keys that protects blockchain data. Every user on the network has two keys: a public key, which is like an address that anyone can see, and a private key, which is like a password that only the owner should know.

Your private key makes the digital signature we talked about before when you send crypto. Your public key can be used by the network to check the signature, but no one can figure out your private key from the public one. This one-way math is what keeps blockchain transactions safe without needing a central authority to confirm who is who.

Keep your private key safe, just like you would your bank account PIN. If you lose it, you can’t get to your assets. Give it to someone else, and they will be in charge. The math is always right, but the weakness is usually human error, not a flaw in the math.

Smart Contracts and Automation

Smart contracts are tiny pieces of software that live on the blockchain and run on their own when certain conditions are met. You put in the right amount of money, press a button, and the product drops out of a vending machine. No need for a cashier. The same goes for smart contracts, but the “products” can be payments, asset transfers, insurance payouts, or just about anything that can be put into an if/then rule.

The code for a smart contract becomes part of the blockchain when it is deployed, so the terms can’t be changed after the fact. This cuts out the need for middlemen and speeds up processes that used to take lawyers, escrow agents, or manual sign-offs.

Smart contracts are already being used to run NFT marketplaces, decentralized finance (DeFi) platforms, and automated supply-chain workflows. As the technology gets better, they’re going to automate even more of the little problems that come up in business every day.

Advantages of Blockchain Technology for Businesses and Users

How Blockchain Security Builds User Trust

You usually have to work hard for years to earn trust. Blockchain skips that timeline. Because a distributed network cryptographically signs and checks every transaction, there is no one person who could change the books. People, businesses, and even competitors can all use the same ledger and trust the same data without having to take each other’s word for it.

That means companies will have to do fewer costly audits and spend less time reconciling records that don’t match. For regular people, it means being sure that no one has messed with your personal and financial records. People stop trusting reputation and start trusting math, which doesn’t pick sides.

Transactions that are faster and cheaper

Traditional payments, especially those made across borders, go through a series of banks, clearinghouses, and processors, each of which takes a cut and adds time. It can take days and cost a lot in fees to send money by wire.

Blockchain cuts out most of those middlemen. Once a transaction is confirmed on-chain, it settles almost right away. That speed is especially important for global trade and cross-border payments, where the old system was the slowest and most expensive.

This is also a big part of why InstaXchange can process crypto transactions so quickly. Users benefit directly from the underlying technology that can move value in minutes instead of days because they can get to their money faster and pay less.

Better ability to track and audit

Every entry on a blockchain has a permanent timestamp and a clear link to the entries that came before and after it. That leaves a trail of evidence that never ends for anything that is tracked on the network.

Supply chain managers use this feature to follow raw materials from the farm or mine to the store shelf where the finished product is. It helps financial compliance teams make clean audit trails much faster than they could with paper records or databases that aren’t connected. In both cases, the blockchain doesn’t just show you what happened; it also shows you when it happened and in what order, and you can’t change it after the fact.

This level of traceability cuts down on fraud, catches mistakes early, and makes sure that everyone is responsible for the same version of events.

Financial Inclusion and Global Access

There is a problem with traditional banking that keeps people out. Hundreds of millions of people around the world don’t have access to even a basic bank account, let alone investment tools or insurance products. Blockchain isn’t concerned about business hours, borders, or credit scores.

Anyone with an internet connection can join a blockchain network, send and receive money, and use decentralized financial services. For people who live in areas with few banks, that’s a real game-changer. There are no geographic limits on blockchain-based payment systems, which run all day, every day of the year.

InstaXchange was made with this ease of use in mind so that anyone, anywhere, can buy and sell cryptocurrency without having to deal with a lot of red tape.

Blockchain Challenges and Opportunities

Energy Consumption and Sustainability Solutions

Let’s get right to the point: Proof of Work blockchains use a lot of electricity. It doesn’t take long for the computing power needed to solve those cryptographic puzzles to add up, and critics are right to point out the environmental cost.

The good news is that the industry is working hard to find more environmentally friendly options. Proof of Stake cuts down on energy use by a lot. Hybrid models and off-chain processing methods are cutting down on use even more. As these methods become more popular, blockchain is slowly closing the gap between how safe it is and how much energy it uses.

Making transactions faster and easier to scale

The main goal of early blockchains was to keep things safe, and speed was a secondary goal. Bitcoin, for example, can only handle a few transactions per second. This is fine for a digital store of value, but not nearly enough for a global payment network. When demand goes up, fees go up and confirmation times get longer.

Developers are dealing with this directly in a number of ways. Layer-two protocols group transactions that happen off-chain and send summaries back to the main blockchain. This helps ease congestion. Sharding divides the network into parallel parts so that different groups of nodes can handle different transactions at the same time. More efficient consensus algorithms make existing hardware work faster.

Getting around legal and regulatory problems

Blockchain was made to work outside of traditional systems, which makes it hard for regulatory frameworks that are based on centralized oversight to work with it. How do you tax an asset that isn’t centralized? When a smart contract goes wrong, who is to blame? These are things that governments are still trying to figure out.

The uncertainty can make it take longer for people to adopt, especially for big companies that need to know they are on solid legal ground before putting money into something. But things are getting better. Regulators in many countries are making their rules clearer, and groups from the industry are working with policymakers to create rules that protect consumers without stifling new ideas.

Balancing Data Privacy and Transparency

One of the best things about blockchain is that it is open and honest. But this can also be a bad thing. How do you keep private or business information safe if every transaction is always visible?

This is most directly a problem for public blockchains. Zero-knowledge proofs and other cutting-edge cryptographic methods are helping to find the answer. These methods let one party prove something is true (like that they have enough money) without giving away the data that supports it. Selective disclosure methods let users choose exactly what they share and with whom.

These improvements are making it possible to enjoy blockchain’s ability to be verified without giving up privacy, which is necessary for widespread use.

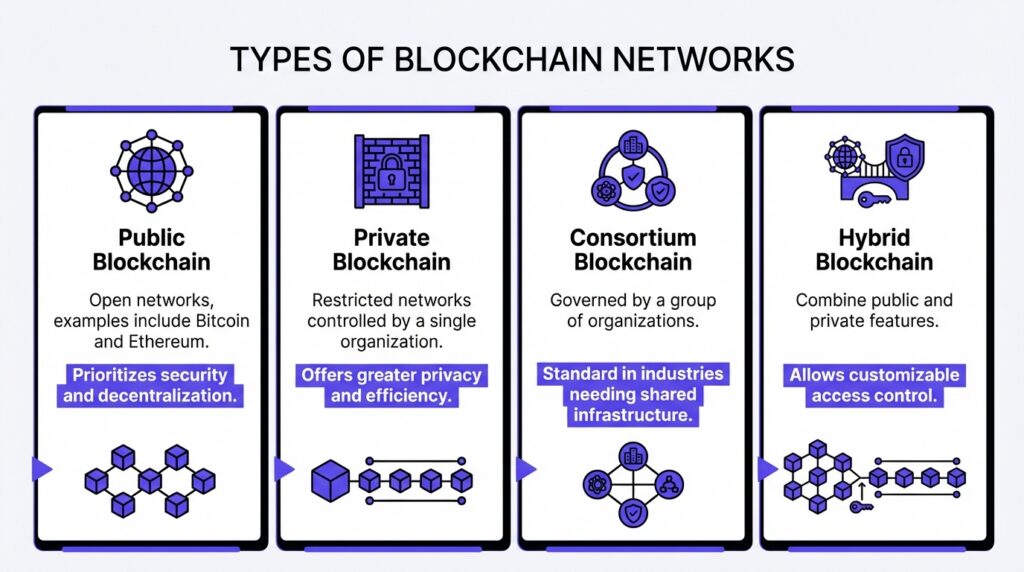

Types of Blockchain Networks

Public Blockchain

Anyone can see everything on public blockchains. Anyone can join, see transactions, and help with validation. Bitcoin and Ethereum are two of the most famous ones. They tend to process transactions more slowly than private ones because they put security and decentralization first. However, they offer the most censorship resistance and openness.

Most cryptocurrency trading, including the assets you can buy on InstaXchange, is based on public blockchains. Their openness encourages new ideas, but it also makes it harder to scale and keep things private, which developers are still working on.

Private Blockchain

Private blockchains are networks that only certain people can join and are run by one organization or a small group of approved participants. The entity in charge decides who can read, write, or check data. Transactions can be confirmed faster and with more predictable performance because there are fewer nodes involved.

Companies like private blockchains for things like coordinating the supply chain, keeping private records, and sharing data between departments. There is less decentralization, but for industries that need strict control and compliance, this is often an acceptable trade-off.

Consortium Blockchain

A consortium blockchain is positioned between public and private blockchains. A group of organizations that work together to keep the network running manages it. No one member has complete control; instead, each partner runs one or more nodes.

This setup is excellent for industries where competitors need to work together on shared data without giving up their own private information. Banking alliances, logistics networks, and healthcare data exchanges often use consortium models to get the benefits of blockchain—trust, transparency, and automation—without letting everyone see the network.

Hybrid Blockchain

Hybrid blockchains have both public and private parts. Sensitive data and core operations stay on a permissioned chain that only authorized users can access. On the other hand, a public chain posts proof of authenticity, certifications, or key milestones that anyone can check.

This design gives businesses the best of both worlds: the privacy they need for everyday tasks and the ability to prove their claims to the public. For this reason, trade finance, government registries, and large-scale enterprise data platforms are using hybrid models more and more.

The Mechanics Behind Blockchain Functionality

How Blocks Communicate Within the Network

A new transaction doesn’t go to a central hub when it is made. Instead, it spreads across the peer-to-peer network in a process known as gossip propagation. Each node that receives the transaction checks it and sends it to its neighbors until everyone on the network knows.

A Merkle tree is a data structure that organizes transactions inside each block. A Merkle tree lets any node quickly check that a transaction is in a block by looking at just a small piece of data instead of the whole block. This approach keeps the network running quickly and well, even when there are more transactions.

Synchronization and Data Integrity Across Nodes

Each node checks the accuracy of a proposed block of transactions before accepting it. The network automatically rejects any version that a node presents that is different from the majority. The chain that everyone agrees on always wins.

Each block contains the cryptographic hash of the previous block, so even the smallest unauthorized change creates a fingerprint that doesn’t match and is flagged immediately. Data integrity isn’t up to one watchdog; it’s up to a network of distributed mathematical checks that run at the same time across the whole network.

How Consensus Keeps the Network Safe

Any blockchain’s security depends on consensus mechanisms. They say how people agree on which transactions are valid, how they should be recorded, and who gets to suggest the next block.

Proof of Work protects the network by requiring a lot of computing power, which makes it hard to attack but also hard to run. Proof of Stake keeps it safe by giving validators money on the line, so cheating costs them money directly. Newer designs, like delegated proof-of-stake and hybrid models, try to find the right balance between decentralization and performance.

Every method of reaching a consensus involves trade-offs. Proof of Work uses a lot of energy. Proof of Stake can give rich people more power over others. The blockchain community is always working to improve these systems, and each new generation makes the technology stronger.

Why Transparency Builds Trust in Blockchain Systems

When every transaction is timestamped, publicly tracked, and verified by multiple parties, trust is a fact, not an opinion. Users don’t have to trust that the records are correct; they can check for themselves.

In practice, this technology gets rid of a whole group of middlemen. Companies can work together across borders using a shared ledger that both sides agree is correct. This way, they don’t have to hire auditors or set up costly reconciliation systems.

Of course, total openness presents challenges; it is crucial to safeguard sensitive data that requires privacy. That’s why modern blockchains now come with zero-knowledge proofs and other cryptographic tools that let users check claims without revealing the details behind them.

Limitations and the Way Forward

Blockchain is not a universal solution. Every node that stores every transaction is great for security but bad for throughput. You can tell when the network is busy because transaction fees go up and confirmation times go down.

The industry’s answer is complex. Layer-two solutions, sidechains, and sharding all work on the bottleneck in different ways, taking some of the work off the main chain without weakening its core guarantees. Blockchain is becoming faster, cheaper, and more useful for everyday use as these technologies get better. This means that more and more people can benefit from its key features of decentralization, immutability, and transparency.

Conclusion: Why the evolution of blockchain is important

Since its initial use to create a digital currency, blockchain has undergone significant changes. Today, almost every major industry needs to know how blockchain works. For example, finance uses it for instant settlement and lower operational risk, supply chains use it for end-to-end traceability, and governments are looking into it for public records that can’t be tampered with.

The main promise is still a system where trust is built into the technology, not based on any one organization’s goodwill. That promise is becoming more accessible to more people as scalability gets better, rules get clearer, and privacy tools get better.

We at InstaXchange think that the first step to making better choices in the crypto space is to learn how blockchain works. Knowing the tech behind your purchases, whether it’s your first or five hundredth, will boost your confidence.

FAQ

Who Invented Blockchain?

A person or group using the name Satoshi Nakamoto came up with the idea in 2008. It looked like the system that Bitcoin was built on: a way to keep track of money transactions without a central authority. Nakamoto was the first to put together distributed databases and cryptographic hashing into a working, decentralized ledger. Prior to his work, other researchers had only examined specific aspects of the puzzle. Nakamoto’s true identity remains unknown, but the publication of the Bitcoin white paper marked a pivotal moment in the transition of blockchain from a theoretical concept to a tangible reality.

Can Blockchain Be Hacked?

The blockchain itself is very hard to hack. Changing any recorded data would mean recalculating the hashes for that block and every block after it, which would use up most of the network’s computing power at the same time. That is very unlikely to happen on a big public blockchain.

When breaches do happen, they happen at the edges, where private keys aren’t well protected, smart contracts have bugs, and third-party services are weak. The best ways to protect yourself are to keep your keys safe and use trusted platforms like InstaXchange.

What Are the Main Uses of Blockchain Today?

Blockchain is now used in a wide range of applications beyond cryptocurrencies. Financial institutions use it for faster and more transparent settlement of payments and securities. Supply chains employ it to trace goods and verify authenticity. In healthcare, it facilitates the secure sharing of patient records, while governments utilize it to enhance transparency in identity systems and voting processes.

Other notable uses include digital asset tokenization, decentralized finance (DeFi), and data authentication for intellectual property. The technology’s flexibility enables it to serve as both a financial infrastructure and a reliable means of recording and verifying information across industries.

Is Blockchain the Same as Bitcoin?

Blockchain and Bitcoin are closely related but not identical. Blockchain is the underlying technology, a distributed ledger that securely and transparently records data. Bitcoin is one specific application of that technology, designed to enable peer-to-peer digital payments without intermediaries.

In simple terms, Bitcoin uses blockchain technology, but blockchain itself can support numerous systems beyond digital currencies, including smart contracts, data registries, and decentralized applications.

How Does Blockchain Actually Work?

Blockchain works by distributing data across a network of computers, known as nodes, that collectively validate and record transactions. When a new transaction occurs, it is encrypted and broadcast to the network. Nodes verify their authenticity using cryptographic rules and then group valid transactions into blocks.Each block includes a timestamp and a cryptographic link to the previous one, creating a continuous chain that cannot be altered without consensus from the majority of participants. This decentralized design eliminates the need for intermediaries, ensuring that all records remain transparent, secure, and verifiable over time.